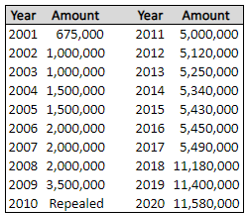

estate tax unified credit history

A deceased spousal unused exclusion amount may not be taken into account by a surviving spouse under paragraph 2 unless the executor of the estate of the deceased spouse files an estate tax return on which such amount is computed and makes an election on such return that such amount may be so taken into account. As an overview the unified credit for estate and lifetime gift tax purposes is currently 5340000 per person.

![]()

Estate Tax Rate Schedule And Unified Credit Amounts Download Table

During this time someone could give away up to 30000 per year and 60000 upon death.

. And 47000 in 1981. Gift and Estate Tax Exemptions The Unified Credit. Estate tax history was 40000 from 1935 to 1942.

Most relatively simple estates cash publicly traded securities small amounts of other easily valued assets and no special deductions or elections or jointly held property do not require the filing of an estate tax return. The unified gift and estate tax exclusion for 2011 and 2012 is 5000000 which is equivalent to a tax credit of 1730800. In the case of estate and gift taxes the unified tax credit provides a set amount that any individual can gift during their lifetime before any of these two taxes apply.

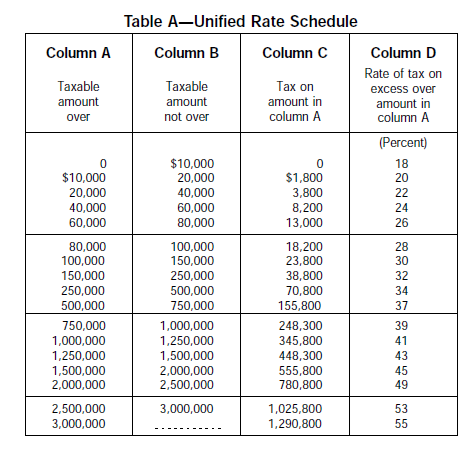

The unified tax credit is an exemption limit that applies both to taxable gifts you gave during your life and the estate you plan to leave behind for others. After 1987 the estate tax was paid by no more than three-tenths of one percent in a given year. The credit to be applied for purposes of computing As estate tax is based on the 68 million basic exclusion amount as of As date of death subject to the limitation of section 2010d.

A person giving the gifts has a lifetime exemption from paying taxes on those gifts until they reach a certain figure. A key component of this exclusion is the basic exclusion amount BEA. If youd prefer to give away more of your assets while still alive in the form of gifts to loved ones you can pull from this unified credit and avoid paying additional taxes on those monetary gifts in the year you gave.

Prior to the 1976 Act estate taxes were paid by approximately seven percent of estates in any given year. Amount of Unified Credit 2001-2009 Year of death Credit 2001 220550 2002 345800 2003 345800 2004 555800 2005 555800 2006 780800 2007 780800 2008 780800 2009 1455800 Source. The estate and gift taxes for example have shared a unified rate schedule since they were combined in 1976 and given the name Unified Transfer Tax.

Then there is the exemption for gifts and estate taxes. 2 The Tax Reform Act of 1976 replaced the exemption with a unified credit. Unfortunately the provisions sunset in 2011 and the estate tax reverts back to the 1997 law with a top rate of 55 percent and a unified credit of.

Two recent tax Acts have partially reversed some of the changes made by the 1976 1981 and 1986 Acts. For 2021 that lifetime exemption amount is 117 million. This is called the unified credit.

A unified credit equal to the estate tax liability on the filing threshold in effect for the decedents year of death is allowed for every dece-dent dying after December 31 1976. Such election once made shall be irrevocable. For example if a person with a taxable estate of 6000000 and no lifetime taxable gifts dies in 2011 the estate tax on the persons estate is the tentative tax on 6000000 minus 1730800.

The tax is then reduced by the available unified credit. In general the Gift Tax and Estate Tax provisions apply a unified rate schedule to a persons cumulative taxable gifts and taxable estate to arrive at a net tentative tax. The lowest exemption in US.

From 1916 to 2007 the estate tax exemption gradually rose until it reached 2 million in 2007. Unified Tax Credit. This means that a person can gift during their lifetime or at death up to this amount without implication of an estate or gift tax or some combination of the two.

The unified credit legislation began in 1976. What is the history of the unified gift and Estate Tax Credit. A tax credit that is afforded to every man woman and child in America by.

Internal Revenue Service Instructions for Form 706 - United States Estate and Generation-Skipping Transfer Tax Return various years. That is the estate tax is 2080800. Credits are also allowed for death taxes paid to States and other countries as well as for any gift taxes the decedent may have paid during his or her lifetime.

Individual Bs predeceased spouse C died before 2026 at a time when the basic exclusion amount was 114 million. Any tax due is determined after applying a credit based on an applicable exclusion amount. Intitially this credit was set at 30000 then i t Intitially this credit was set at 30000 then i t increased to 34000 in 1978.

This also includes GSTT gifts generation-skipping transfer tax gifts which are gifts to those more than one.

Gift Tax Exemption Lifetime Gift Tax Exemption The American College Of Trust And Estate Counsel

2017 Estate Tax Rates The Motley Fool

It May Be Time To Start Worrying About The Estate Tax The New York Times

History Of The Unified Tax Credit Apple Growth Partners

The Rise Of The Older Single Female Home Buyer Single Women Real Estate Trends Unmarried Women

U S Estate Tax For Canadians Manulife Investment Management

Housers The First Real Estate Investment Platform Faq S For Investors

Pdf Inheritance Tax Regimes A Comparison

Historical Look At Estate And Gift Tax Rates Wolters Kluwer

A Guide To Estate Taxes Mass Gov

What Happened To The Expected Year End Estate Tax Changes

Housers The First Real Estate Investment Platform Faq S For Investors

2

New York Estate Tax Everything You Need To Know Smartasset

Historical Estate Tax Exemption Amounts And Tax Rates 2022

Historical Estate Tax Exemption Amounts And Tax Rates 2022

2021 Tax Laws Federal Tax Updates Maryland Estate Taxes Mcnamee Hosea

Inheritance Tax Regimes A Comparison Public Sector Economics

U S Estate Tax For Canadians Manulife Investment Management